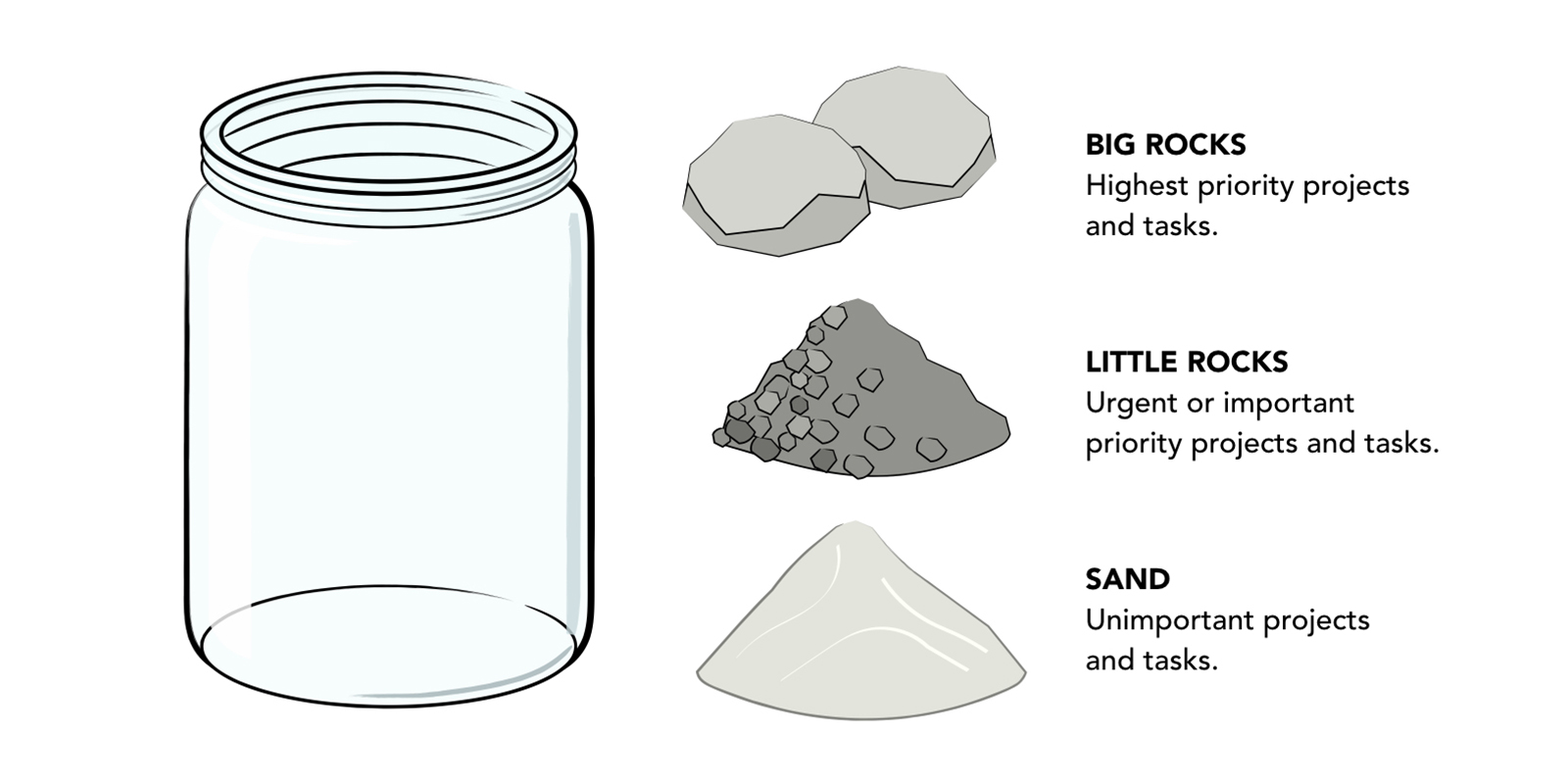

Say you have some rocks, a bunch of pebbles, and some sand, and your goal is to fit as much of everything as you can into a wide-mouth jar. If you start with the sand and then the pebbles, the jar will run out of room for all the rocks. But when you start with the rocks, add the pebbles, and save the sand for last, the sand fills the space between the rocks, and everything fits.

The above anecdote is known as Covey’s Big Rocks theory and states that the most important things need to get done first, or they won’t get done at all.1 Sometimes innovation is more about what you aren’t doing than what you are doing. So how should you decide where to invest your time with innovation initiatives? The answer lies in an innovation strategy.

Operational effectiveness is not strategy

Across the Architecture, Engineering and Construction (AEC) industry, there are vast differences in how well companies execute basic tasks. The performing of these tasks better than how rivals perform them is known as operational effectiveness.2 Operational effectiveness is a direct result of a commoditising market whereby organisations seek to make productivity gains. For many AEC organisations, operational effectiveness is their panacea – the remedy for all difficulties. It is seductive because it is concrete and actionable.

However, because these organisations are doing the same as their competitors, albeit better, they are undifferentiated. Consequently, this often means they have to pass the benefit on to the client in the form of lower prices. In so doing, they lose the ability to create attractive returns and initiate the downward spiral of increasingly commoditised offerings they sought to avoid.3 Put simply, competition based on operational effectiveness alone is mutually destructive, leading to wars of attrition that can be arrested only by limiting competition.

While improving operational effectiveness is a necessary part of management, it is not strategy. Whereas operational effectiveness means performing similar activities better than rivals, strategic positioning means performing different activities from rivals or performing similar activities differently.4 In other words, competitive strategy is about being different.

The innovation premium

It is our choices, Harry, that show what we truly are, far more than our abilities.

Professor Albus Dumbledore in J K Rowling5

Without innovation, offerings become more and more like each other. They commoditise. Innovations’ greatest value is when it differentiates us from our competitors sufficiently that clients prefer our offers to theirs and will pay a premium to support that preference. Within architecture, we see this innovation premium with architects such as Norman Foster ($240m net worth), Frank Gehry ($100m net worth), and the late Zaha Hadid ($95m net worth). These starchitects made their name and wealth by being different to their peers, not by doing the same tasks more efficiently.

Efficiency is the enemy of innovation

But when it comes to design technology, the narrative is often centred on “eliminating the boring and repetitive tasks so that the user can focus on more importing things.” While eliminating rote tasks is a step forward, this attitude is a missed opportunity to achieving true innovation. It is filling the jar with unimportant sand instead of the high-priority big rocks.

Some may argue that operational effectiveness is the vehicle to enable true innovation. However, the very processes and values that constitute an organisation’s capabilities in one context define its disabilities in another context. Put simply, efficiency is the enemy of innovation. Innovation initiatives frequently fail, as efficient firms simply do not allow for a culture of waste, which is required when trying to imagine and create the future.6 How, then, do organisations and their employees know which to focus on and when? In a world where almost anything is possible, the question is not “Can it be done” but “Should it be done”.

Thinking differently

In 2016, the World Economic Forum claimed that 65% of children entering primary school will ultimately end up working in completely new job types that don’t yet exist.7 Each successful bit of automation will generate new occupations and jobs we didn’t know we wanted done. Given the inevitable technological convergence underway, thinking differently will be the source of innovation and wealth, not the automation of rote tasks. As Kevin Kelly suggests, “Our most important mechanical inventions are not machines that do what humans do better, but machines that can do things we can’t do at all.”8 Good organisations know to put their best employees on their best opportunities, not their biggest problems. The same is true for innovation. Every day spent on operational effectiveness is another day not spent on innovation.

An innovation strategy

An innovation strategy is a coherent set of processes that dictates how an organisation searches for novel problems and solutions, synthesises ideas into a business concept and selects which projects get funded. An explicit innovation strategy helps you understand which initiatives might be a good fit for your organisation and navigate the inherent trade-offs.9 So, how do you decide what is a good fit?

As Geoffrey Moore, the American organisational theorist, explains, “Managing innovation requires executives to foster a bottom-up stream of innovation opportunities, but at the same time to commit top down to a single innovation vector along which separation will be gained. Once that commitment is made, other forms of innovation are expected to align with or subordinate themselves to the chosen vector.”10 In other words, management must define what matters to them and make it explicit. How many organisations can claim their employees are crystal clear on the organisation’s vision and can articulate it?

Rethinking business as usual

Without an explicit strategy indicating otherwise, organisational forces will tend to drive initiatives into the operational effectiveness zone. To illustrate this point, consider a recent discussion we had with a potential client. Senior management were interested in the organisation becoming more innovative to keep up with their competitors. Everything was on the table. We discussed emerging trends and technologies. We also discussed what their competitors were working on and the time and financial investment they had put into said initiatives. By the end, there was a long shopping list of possible initiatives. There was no right or wrong answer, of course. It was merely working out which initiative most aligned with the organisation’s vision and executing it.

Fast forward a few weeks, and the conversation quickly regressed to solving rote tasks in Revit. The very same problems that many other organisations had already solved. My dismay wasn’t that these initiatives were operational effectiveness based. Organisations should be trying to do things better through marginal gains and continuous improvements. Rather, my concern was that for this organisation, the two words were interchangeable. Operational effectiveness meant innovation, and innovation meant operational effectiveness. Semantics aside, it meant they were focusing on business as usual but under the guise of innovation. It was innovation theatre.

The innovation cornucopia

At the other end of the spectrum, some organisations explore every shiny, new technology currently in vogue – a kind of innovation cornucopia. Unfortunately, the consequence of this approach is often a lot of quick exploratory studies that fail to deliver significant, long-term advantages. Sometimes this stems from overzealous employees wanting to experiment without oversight, resulting in incomplete and unused initiatives. Other times, it comes from senior management conveying that every initiative is important. They start new initiatives without stopping other activities or simultaneously start too many initiatives.11 Either way, the root of the problem stems from a lack of an explicit innovation strategy. When we try to focus on everything, we focus on nothing. An innovation strategy defines where and how we should approach opportunities.

The monkey and the pedestal

Imagine you want to get a monkey to recite Shakespeare while sitting on a pedestal. What do you do first – train the monkey or build the pedestal? Training the monkey will be hard, so maybe we should start with the pedestal. When our boss checks in, we can demonstrate measurable progress and assure them we’re on the right track.

But this is innovation theatre. If we can’t get the monkey to recite Shakespeare on the ground, then all the time and energy put into crafting the pedestal was wasted. The parable comes from Astro Teller, the head of X, Google’s moonshot division. The premise is the same as Covey’s Big Rock theory – prioritise and tackle the most difficult and important tasks first.12

Fail fast

Innovation, by nature, is the exploration of the unknown, so if we’re going to fail, we want to fail fast. Innovation should be seen as a learning framework designed to test assumptions and unearth unknowns. Every organisation will have a different tolerance to risk, but this needs to be considered along a broad spectrum of risk and reward – and without bias.

Loss aversion bias

Consider the following problems:

Problem 1: Which do you choose?

Get $900 for sure OR 90% chance to get $1,000

Problem 2: Which do you choose?

Lose $900 for sure OR 90% chance to lose $1,000

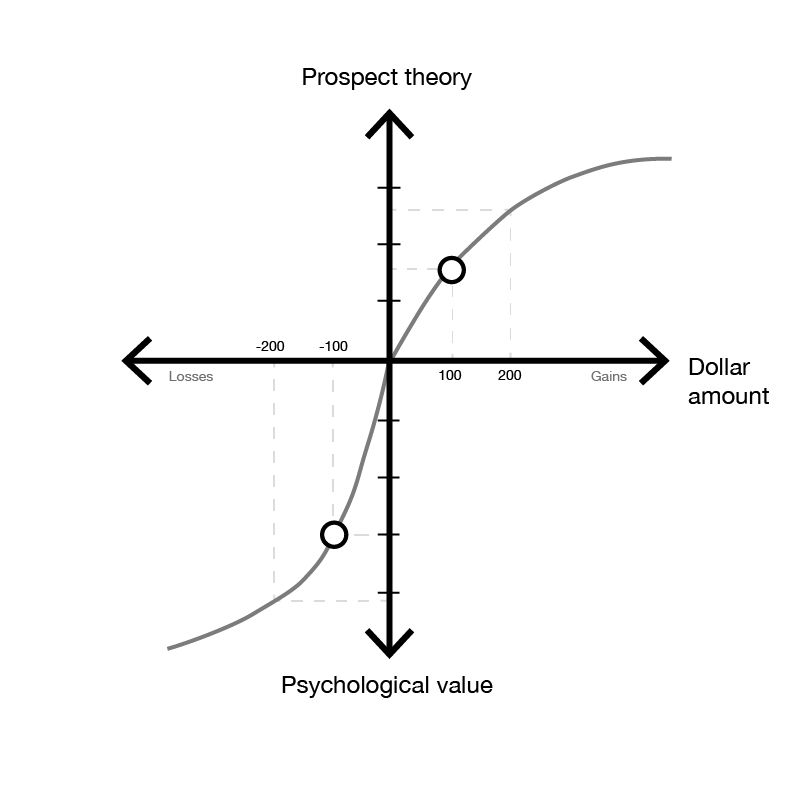

Mathematically, both questions are the same. However, when framed as a gain (problem 1), most people take the sure thing. But when framed as a loss (problem 2), most people take the gamble. This is known as the loss aversion bias, and it’s the tendency for people to strongly prefer avoiding losses to obtaining gains.13

Loss aversion ratio

The research of the Nobel Prize winner Daniel Kahneman sheds further light on the systemic biases we have when it comes to loss aversion. Consider this problem:

Problem 3: You are offered a gamble on the toss of a coin.

If the coin shows tails, you lose $100.

If the coin shows heads, you win $150.

Is this gamble attractive? Would you accept it?

To make the choice, you must balance the psychological benefit of getting $150 against the psychological cost of losing $100. Although the expected value of the gamble is obviously positive, for most people, the fear of losing $100 is more intense than the hope of gaining $150.14 We can measure the extent of your loss aversion by asking a simple question:

What is the smallest gain that I need to balance an equal chance to lose $100?

Kahneman’s research shows that for many people, it is about $200, twice as much as the loss. This is known as the loss aversion ratio, and it is usually in the range of 1.5 to 2.5.15

The loss aversion bias comes into play when establishing an innovation strategy, as people have a tendency to focus on the cost (loss), rather than the value (gains) when making decisions. An explicit innovation strategy can help counteract the bias, as initiatives can be properly evaluated in terms of their potential.

A portfolio approach

Innovation means saying no to one thousand things.

Steve Jobs16

There are different schools of thought about how organisations should invest in innovation. For example, Jim Collins argues, “The most effective investment strategy is a highly undiversified portfolio when you are right.”17 Geoffrey Moore agrees, claiming that taking a smorgasbord approach to innovation types reduces rather than increases differentiation.18 Putting all of your eggs in the same basket, so to speak, does come with higher risk. The main benefit, however, is focus. With each turn of the flywheel, momentum builds, building deeper and deeper expertise.

The alternative is a portfolio approach in keeping with your risk appetite. Once you have gathered a range of possible innovations, take a holistic view of the entire innovation portfolio to get a clear picture of how the initiatives fall on the risk spectrum. This gives managers a way to discuss and balance the portfolio.19 Kanter, for example, suggests the innovation pyramid where big bets at the top get the most investment and a broad base of incremental innovations at the bottom.20

When selecting which opportunities to pursue, staff may become disgruntled that their idea wasn’t chosen. However, I like David Weinberger’s notion of filters. In his book Too big to know, he suggests that “Filters no longer filter out. They filter forward, bringing their results to the front. What doesn’t make it through a filter is still visible and available in the background.”21

Four essential tasks

There are four essential tasks in creating and implementing an innovation strategy. The first is to answer the question, “How are we expecting innovation to create value?” and then explain that to the organisation. The second is to create a high-level plan for allocating resources to the different kinds of innovation. Ultimately, where you spend your money, time, and effort is your strategy, regardless of what you say.

Ultimately, where you spend your money, time, and effort is your strategy, regardless of what you say.

The third is to manage trade-offs. Because every team and department will naturally want to serve its interests, the innovation strategy should clarify what is best for the whole company. The final task is recognising that innovation strategies must evolve. Like the innovation process, an innovation strategy involves continual experimentation, learning, and adaptation.22

Conclusion

Everyone will have an opinion about the next big technological disruptor, but what is clear is that companies need to be smarter if they are to succeed. AEC organisations are full of pedestals, with relatively few monkeys. Rote tasks are automated, and the latest version of software deployed. We convince ourselves we’re building the infrastructure to enable others to innovate. But the hard, wicked problems – like designing better buildings – remain untouched. We run out of time or get distracted by the next quick win. We must put aside the illusion of progress and focus on Doing Better Things. We must forget the pedestal and focus on the monkey. Ideas are easy. Execution is everything. And to execute well, you need an innovation strategy.

References

1 Covey, S. (2020). The 7 habits of highly effective people. Simon and Schuster.

2 Porter, M. (2011). What is strategy. In HBR’s 10 must reads on strategy. Harvard Business Review Press, Boston, p.2.

3 Moore, G. (2008). Dealing with Darwin: How great companies innovate at every phase of their innovation. Penguin Books, London, p.242.

4 Porter, M. (2011). What is strategy. In HBR’s 10 must reads on strategy. Harvard Business Review Press, Boston, p.2.

5 Rowling, J. (2004). The chamber of secrets. Bloomsbury Publishing, London, p.358

6 Enns, B. (2018). Pricing creativity. A guide to profit beyond the billable hour. Rockbench Publishing, Nashville, p.24.

7 World Economic Forum. (18 Jan 2016). The future of jobs: Employment, skills and workforce strategy for the Fourth Industrial Revolution.

8 Kelly, K. (2017). The inevitable: Understanding the 12 technological forces that will shape our future. Penguin Books, New York, p.47.

9 Pisano, G. (June 2015). You need an innovation strategy. Harvard Business Review, Boston.

10 Moore, G. (2008). Dealing with Darwin: How great companies innovate at every phase of their innovation. Penguin Books, London, p.59.

11 Heifetz, R. & Laurie, D. (2011). The work of leadership. In HBR’s 10 must reads on leadership. Harvard Business Review Press, Boston, pp.64-65.

12 Teller, A. (28 Oct 2016). Astro Teller on Moonshots for Alphabet’s X. In The Wall Street Journal Video.

13 Kahneman, D. (2011). Thinking, fast and slow. Penguin Books, Great Britain, pp.279-280.

14 Kahneman, D. (2011). Thinking, fast and slow. Penguin Books, Great Britain, p.283.

15 Kahneman, D. (2011). Thinking, fast and slow. Penguin Books, Great Britain, p.284.

16 Jobs, S. (1997). Apple Worldwide Developers Conference.

17 Collins, J. (2001). Good to great: Why some companies make the leap…and others don’t. Random House, London, p.141.

18 Moore, G. (2008). Dealing with Darwin: How great companies innovate at every phase of their innovation. Penguin Books, London, p.28.

19 Nagji, B. & Tuff, G. (May 2012). Managing your innovation portfolio. Harvard Business Review Press, Boston.

20 Kanter, R. (2013). Innovation: The classic traps. In HBR’s 10 must reads on innovation. Harvard Business Review Press, Boston, p.108.

21 Weinberger, D. (2014). Too big to know: Rethinking knowledge now that the facts aren’t the facts, experts are everywhere, and the smartest person in the room is the room. Basic Books, New York, p.11.

22 Pisano, G. (2015). You Need an Innovation Strategy. Harvard Business Review Press, Boston.